You've probably seen mortgage deals advertised with a minimum deposit of just 5%, and that figure is the starting line for most first-time buyers. It’s the key that gets your foot on the property ladder. But in reality, the amount you'll actually need can be a bit more nuanced.

Decoding the Minimum Deposit for a House

Think of a house deposit like a down payment on a car, just on a much bigger scale. It's the chunk of the property’s price you pay upfront from your own savings, with a mortgage lender covering the rest.

This initial payment is absolutely crucial. It proves your financial commitment to the lender and, most importantly, it reduces their risk. The less they have to lend you, the safer their investment feels to them.

You’ll hear the term Loan-to-Value (LTV) thrown around a lot, and it’s simply the relationship between your deposit and your mortgage. It's the percentage of the property's value you need to borrow.

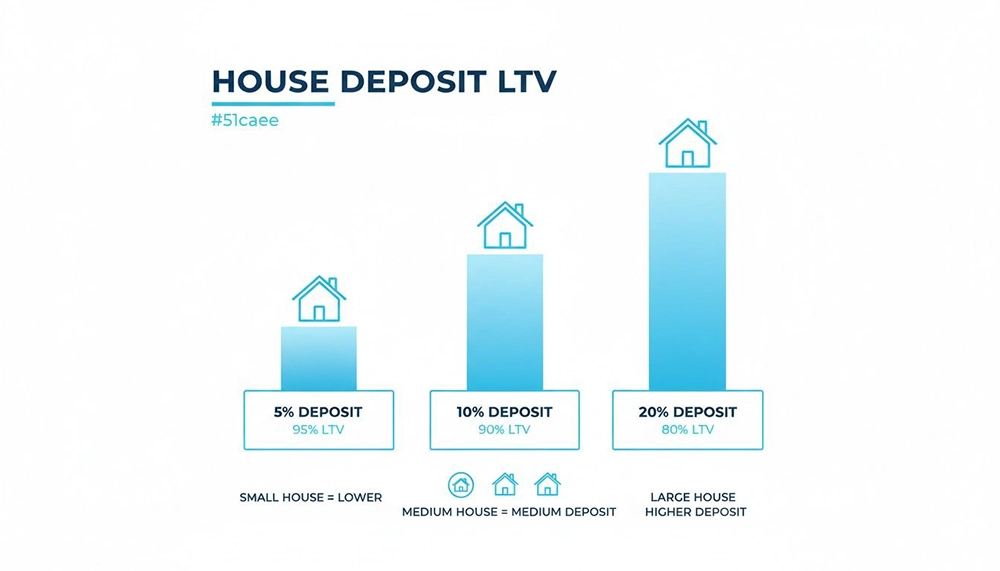

A simple way to think about it: if you're buying a £200,000 house with a £20,000 deposit (which is 10%), your mortgage will be £180,000. That means you're borrowing 90% of the home's value, giving you a 90% LTV. The bigger your deposit, the lower your LTV.

The chart below shows just how different deposit sizes can change the whole picture.

As you can see, a bigger deposit doesn't just mean borrowing less money. It often opens the door to much better mortgage products with lower interest rates, saving you a small fortune over the long run.

Why a Bigger Deposit Always Helps

Pushing yourself to save more than the bare minimum can have a huge impact on your financial future. A lower LTV makes you a far more attractive borrower in the eyes of lenders, which usually means they’ll offer you:

- Lower monthly mortgage repayments.

- A better overall interest rate for the life of the loan.

- A much wider choice of mortgage deals to pick from.

The table below gives a practical look at how this works for a typical £250,000 property. Notice how a larger deposit directly lowers the LTV, making you a less risky borrower.

| How Your Deposit Changes Your Mortgage (For a £250,000 Property) | |||

|---|---|---|---|

| Deposit Percentage | Deposit Amount | Mortgage Amount | Loan-to-Value (LTV) |

| 5% | £12,500 | £237,500 | 95% |

| 10% | £25,000 | £225,000 | 90% |

| 15% | £37,500 | £212,500 | 85% |

| 20% | £50,000 | £200,000 | 80% |

As the LTV drops, lenders see you as a safer bet and are more willing to offer you their most competitive rates.

Saving has become a real challenge, but plenty of people are still making it happen. Recently, there were 341,068 purchases by first-time buyers across the UK, even as the average deposit climbed to a hefty £61,090. This just goes to show how vital strategic saving has become, a topic we cover in our guides for prospective renters looking to make the leap to buying on https://www.roomsforlet.co.uk.

Ultimately, while starting with a 5% deposit is a great first step, aiming for 10% or more will put you in a much stronger financial position when it’s time to buy.

How Lenders See Your Deposit and Your Risk

To really get your head around the minimum deposit for a house, you need to step into a lender's shoes. Imagine a friend asks you for a massive loan. Your first thought would be, "How can I be sure I'll get this back?" That's exactly the mindset of a mortgage lender with every single application they review.

Your deposit is their safety net. It's your "skin in the game," a clear signal of your financial commitment. A bigger deposit means a smaller loan, which instantly makes you a less risky prospect for them. If the worst happened and they had to repossess the property, your deposit cushions their potential loss.

But your deposit is just one piece of the puzzle. Lenders are building a complete financial picture of you, weighing up several factors to decide whether to lend to you and, crucially, what interest rate they’ll offer.

Your Financial Footprint Matters

One of the very first things a lender will dig into is your credit history. A healthy credit score, built from a solid track record of paying bills on time, shows them you’re a reliable borrower. It tells a story of someone who manages their money responsibly and is likely to honour a mortgage commitment.

On the flip side, a history of missed payments or defaults flashes a big red warning light. Lenders see this as a higher risk, which could mean they’ll ask for a much larger deposit or, in some cases, turn down your application altogether.

Key Takeaway: Your financial habits today directly shape your chances of getting a mortgage tomorrow. Lenders use your past behaviour as their best guess for your future reliability.

Your income and job stability are just as important. Lenders need to see a steady, predictable income that can comfortably cover your mortgage payments on top of all your other outgoings.

- Steady Employment: A long-term, permanent job gives them the reassurance that your income is secure.

- Self-Employment: If you're self-employed, they’ll usually want to see at least two to three years of accounts to prove your income is stable.

- Affordability Checks: They will run detailed affordability checks, poring over your bank statements to understand your spending habits and make sure you have enough left over each month.

The Property Itself Influences Risk

Finally, the type of property you’re planning to buy also gets put under the microscope. A standard brick-and-mortar house is usually straightforward, but things can get complicated with non-standard properties.

For instance, a home with unusual construction, like a concrete frame or a thatched roof, might be harder to sell down the line. This makes it a riskier asset for the lender, who could ask for a larger deposit to balance out that risk. As you think about how lenders assess your application, it's a great idea to explore the different mortgage products available, as this can also affect your deposit requirements. Understanding all these variables helps you see your application from their point of view.

The Real Cost of a Deposit Across the UK

While you might hear that the minimum deposit for a house is just 5%, the amount people actually need to save is a totally different story. The biggest factor? Your postcode.

Where you plan to buy will have a massive impact on the size of the deposit you'll need to pull together. The financial mountain you need to climb for a flat in the North East is worlds away from securing a place in London or the South East.

This isn't meant to put you off—far from it. Knowing this is your strategic advantage. Understanding the regional differences is the first step to making smart decisions about where your hard-earned savings will give you the most buying power.

A Tale of Two Regions

The gap between different parts of the UK isn't just a few thousand pounds; it's a chasm. In some areas, saving a 10% deposit is a challenging but achievable goal. In others, that same percentage demands a six-figure sum. This massive disparity is a direct reflection of regional house prices.

Recent figures paint a crystal-clear picture. The average deposit for a first-time buyer in England was £53,414—a hefty amount, though it was actually a drop from the previous year.

But the regional splits are where it gets really interesting. The North East had the lowest average deposit at just £29,740. Compare that to Greater London, where buyers needed an eye-watering average of £108,848. That’s more than three times higher. You can dig into more of these regional trends in this detailed first-time buyer statistics report.

This data highlights a crucial point: being flexible on location can literally shave years off the time it takes to save for a home. If your job allows it, looking at more affordable regions could fast-track your journey to homeownership.

What This Means for Your Savings Strategy

Seeing these numbers laid out helps you shift from a vague, national average to a specific, actionable goal based on where you actually want to live. It makes the whole process feel much more real.

Here’s how you can use this insight:

- Research Your Target Area: Don't just browse house prices. Dig into the average deposit amounts for first-time buyers in the specific towns or cities you’re considering.

- Look at "Commuter Belt" Locations: If you need to be near a major city for work, explore towns with great transport links. A 30-minute train ride could save you tens of thousands of pounds on your deposit.

- Stay Flexible: If you aren't tied to one spot, your deposit will stretch much further in regions like the North West, Yorkshire, or Scotland compared to the South East.

Ultimately, location is one of the most powerful levers you can pull. For anyone struggling to save while paying rent, exploring different areas could be the game-changer. You might find that looking for rooms to rent in a more affordable city for a year or two could seriously turbocharge your savings.

Understanding the real cost across the UK empowers you to build a smarter, more achievable path to getting on the property ladder.

Government Schemes to Help You Buy Sooner

Does it feel like the goalposts for your house deposit keep shifting further down the pitch? You’re definitely not alone. Saving that big lump sum is one of the toughest hurdles on the path to owning your own home.

Recognising this, the government has created several schemes designed to give aspiring buyers a much-needed leg-up. These initiatives are there to bridge the gap, making it possible to get on the ladder with a smaller deposit than you might think.

The need for this kind of support has become more and more critical. Think about this: over the last 50 years, the average deposit for a first-time buyer couple has rocketed from just 5.36% of the house price in 1975 to a projected 20.17% in 2025.

Past schemes like Help to Buy were game-changers, helping over 390,000 people buy a home with just a 5% deposit. This history shows just how vital these programmes are.

Key Schemes to Know About

While some schemes have come and gone, there are still some powerful options available right now to help you shrink that minimum deposit for a house or give your savings a serious boost. Each one works differently and is built for specific situations, so it’s worth seeing which, if any, fits your plans.

Below is a quick overview of the main players helping buyers get the keys to their first home.

Comparing Key Home Ownership Schemes

Here’s a side-by-side look at the main schemes available to help first-time buyers, outlining their core features and who they benefit most.

| Scheme | Minimum Deposit | Who It's For | Key Feature |

|---|---|---|---|

| Lifetime ISA (LISA) | N/A (Savings product) | First-time buyers aged 18-39 | The government adds a 25% bonus to your savings, up to £1,000 per year. |

| Shared Ownership | Typically 5-10% of the share you buy | People who can't afford 100% of a home | You buy a share (e.g., 25%) and pay subsidised rent on the rest, with a much smaller deposit. |

| Mortgage Guarantee Scheme | 5% of the property value | Buyers with small deposits (not just first-timers) | Gives lenders the confidence to offer 95% mortgages by guaranteeing a portion of the loan. |

These schemes can make a real difference, but it's important to understand how they work before diving in.

Important Insight: These schemes aren't free money; they are tools with specific rules, eligibility criteria, and long-term implications. For example, with Shared Ownership, you’ll still need to pay service charges and ground rent on the full property value.

Choosing the right path depends entirely on your personal finances, where you want to buy, and what you’re looking for in a home. For renters trying to make the leap, understanding these options alongside smart saving strategies is the key to success.

Our blog offers more practical tips on navigating the rental market while you save up and prepare for homeownership.

Actionable Tips for Saving a Deposit While Renting

Trying to save for a house deposit while paying rent can feel like you’re fighting an uphill battle. A huge slice of your income disappears into your landlord's pocket each month, making it feel impossible to get any real momentum going. But trust me, it’s not impossible.

The real secret is to flip your thinking. Stop trying to "save what's left" at the end of the month. Instead, pay yourself first. Treat your deposit fund like any other essential bill – one that gets paid the second your salary hits your bank account. This simple change ensures you're consistently chipping away at your goal.

Create a Deposit-First Budget

Most generic budgeting advice just doesn't work for renters because it fails to respect the massive outgoing that is rent. So, forget vague plans and build a 'deposit-first' budget instead. This means you work out a realistic savings amount before you budget for anything else, apart from your rent and essential bills, of course.

The best way to stick to this? Automate everything. Set up a standing order to transfer your savings amount into a separate, high-interest account the day after payday. This takes temptation out of the equation and turns saving into a habit, not a chore.

Top Tip: If you're aged between 18 and 39, look into opening a Lifetime ISA (LISA). The government gives you a 25% bonus on your savings, which can mean up to £1,000 of free money towards your first home every single year. It’s one of the most powerful tools out there for getting your deposit together faster.

Supercharge Your Savings Strategy

Once your automatic savings are sorted, it’s time to find ways to make that gap between your income and expenses even wider. This doesn't mean you have to live on beans on toast for a year; it’s about making smart, strategic changes that really add up over time.

- Optimise Your Living Situation: Could a house share slash your costs? Even moving into a shared place for just a year or two can free up hundreds of pounds a month. Money that can go straight into your deposit fund.

- Review Your Subscriptions: Time for a financial MOT. Go through your bank statements with a critical eye. That gym membership you never use? The streaming services you forgot you had? They're all quietly slowing you down.

- Boost Your Income: To really put your foot on the accelerator, think about bringing in some extra cash. Exploring options like starting a side hustle can generate additional income that you can earmark purely for your deposit.

Every single pound you can redirect towards your deposit is a step closer to leaving the rental cycle for good. With a solid plan and consistent effort, you'll build that minimum deposit for a house much quicker than you might think.

Getting Your Deposit Ready for Completion Day

You’ve done the hard part and meticulously saved your minimum deposit for a house. Now, it’s time to get that money where it needs to go. Preparing to transfer such a significant sum can feel a bit nerve-wracking, but rest assured, it’s a well-trodden path managed by your solicitor.

Just before the contracts are exchanged, your solicitor will get in touch to request the deposit funds. Don’t be surprised when they ask for a lot of paperwork; they are legally required to carry out Anti-Money Laundering (AML) checks to verify exactly where the money came from. It's a standard, crucial step in the process.

Providing Your Proof of Funds

To get through these checks smoothly, you’ll need to show clear evidence of your deposit's origin. The documents you need will depend entirely on how you built up your savings.

- Personal Savings: If it's all your own hard work, you’ll generally need to provide several months of bank statements. These should clearly show the funds building up in your account over time.

- Gifted Deposit: Has a family member kindly helped you out? They will need to provide a signed letter confirming the money is a genuine gift, with no strings attached and no expectation of it being paid back. They’ll also need to supply their own bank statements and proof of ID.

It's a really good idea to get all of this paperwork gathered together well in advance. Having everything ready to go means you won't be the one causing delays at this critical stage.

Once your solicitor has verified your funds and completed their checks, they will provide you with their client account details for the transfer. As a final security step, always call your solicitor's office to confirm these bank details over the phone before you send any money. This helps protect you from potential fraud.

Making this transfer is the very last financial hurdle you need to clear before the property is officially yours.

Got Questions About Your House Deposit?

Diving into the world of mortgages can feel like learning a new language, and deposits are often the first big hurdle. Getting your head around the numbers and the rules is the key to moving forward with confidence. Let's tackle some of the most common questions buyers have about the minimum deposit for a house.

Can I Get a Mortgage With No Deposit in the UK?

Right now, the short answer is almost certainly no. Those 100% mortgages, sometimes called zero-deposit mortgages, are incredibly rare in today's market.

Every so often, a specialist lender might launch a product like this, but they usually come with a big catch, like needing a family member to act as a guarantor for the loan. For the vast majority of us, a deposit of at least 5% is the absolute minimum you'll need to get on the ladder. Lenders see your deposit as your stake in the game—it's a financial cushion for them if house prices were to drop, which is why they see no-deposit loans as such a big risk.

How Does a Gifted Deposit From Family Affect My Mortgage?

This is a really common way for people to boost their deposit, and lenders are completely used to it. As long as it’s a true gift, with no strings attached and no expectation of being paid back, it generally won't cause any problems for your application.

The lender will just need a signed letter from the person giving you the money.

This letter is just a standard part of the process. It needs to confirm who they are, the exact amount they're gifting, and state clearly that it is a non-refundable gift. Crucially, it must also state that they won't have any legal claim or interest in the property you're buying.

Should I Buy With a 5% Deposit or Wait to Save 10%?

Ah, the classic dilemma. The right answer really comes down to your personal finances and what the housing market is doing at the moment.

Putting down a 10% deposit will almost always open the door to better mortgage deals. Lenders will see you as less of a risk and offer you lower interest rates, which means smaller monthly payments and saving a significant amount of money over the years.

But there's a flip side. If house prices in your dream area are climbing quickly, waiting another year to save could mean the price of the home you want goes up. That increase could easily cancel out, or even outweigh, the savings you'd make from a better interest rate. This is where a good mortgage advisor becomes invaluable—they can help you crunch the numbers for your specific situation.

Finding the right place to live while you're saving is a huge part of the puzzle. Rooms For Let can help you find affordable shared accommodation across the UK, making it easier to build that all-important deposit for your first home. Start your search today at https://www.roomsforlet.co.uk.